Futures Market: LME copper opened at $9,829/mt overnight, dipped to a low of $9,798.5/mt during the session, then fluctuated upward to a high of $9,880/mt, and finally closed at $9,864.5/mt, up $71.5/mt or 0.73% from the previous close of $9,793/mt. Trading volume reached 14,286 lots, and open interest stood at 296,460 lots. Overnight, the SHFE copper 2505 contract opened at 80,270 yuan/mt, hit a low of 79,970 yuan/mt during the session, then fluctuated upward to a high of 80,380 yuan/mt, and finally closed at 80,370 yuan/mt, up 260 yuan/mt or 0.32% from the previous close of 80,520 yuan/mt. Trading volume reached 33,634 lots, and open interest stood at 231,565 lots.

[SMM Copper Morning Briefing] News: (1) On Monday, Indonesia's Energy Minister announced that the country will issue a six-month copper concentrate export license to Freeport Indonesia, allowing exports during smelter maintenance. This will also ensure the Indonesian government continues to receive royalties.

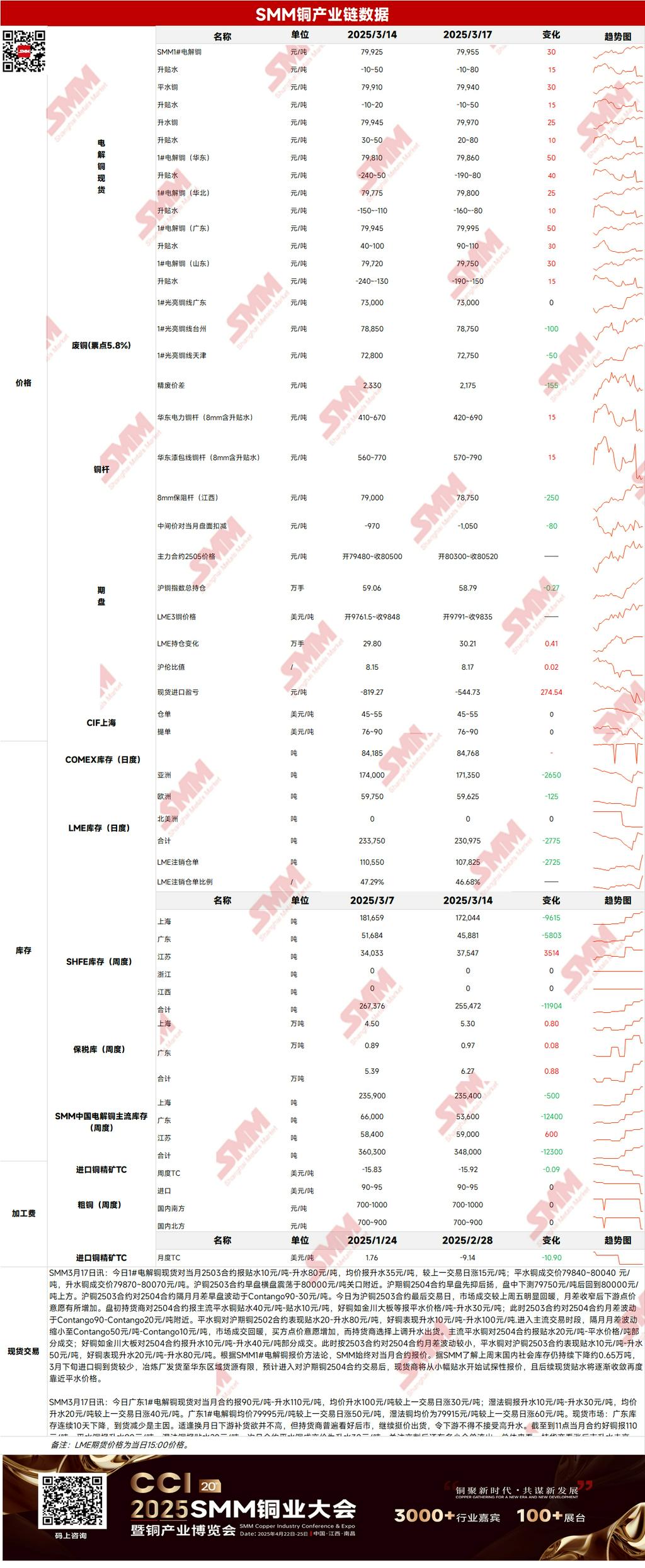

Spot Market: (1) Shanghai: On March 17, mainstream standard-quality copper spot prices against the front-month contract were quoted at a discount of 10 yuan/mt to a premium of 50 yuan/mt, while high-quality copper was quoted at a premium of 20 yuan/mt to 80 yuan/mt. According to SMM, domestic social inventories continued to decline by approximately 6,500 mt over the weekend. With fewer imported copper arrivals in late March and limited shipments from smelters to east China, spot suppliers are expected to start quoting at slight discounts after transitioning to the SHFE copper 2504 contract, with spot discounts gradually narrowing to parity.

(2) Guangdong: On March 17, #1 copper cathode spot prices against the front-month contract were quoted at a premium of 90 yuan/mt to 110 yuan/mt, with an average premium of 100 yuan/mt, up 30 yuan/mt from the previous trading day. Hydro copper was quoted at a premium of 10 yuan/mt to 30 yuan/mt, with an average premium of 20 yuan/mt, up 40 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 79,995 yuan/mt, up 50 yuan/mt from the previous trading day, while hydro copper averaged 79,915 yuan/mt, up 60 yuan/mt. Overall, suppliers were optimistic about rising premiums, but actual transactions on the contract rollover day were moderate.

(3) Imported Copper: On March 17, warrant prices ranged from $45/mt to $55/mt (QP March), with the average price unchanged from the previous trading day. B/L prices ranged from $76/mt to $90/mt (QP April), with the average price also unchanged. EQ copper (CIF B/L) was quoted at $15/mt to $25/mt (QP March), with the average price unchanged. Quotes referenced cargo arrivals in mid-to-late March and early April. Morning spot offers were sparse, with buyers focusing on warrants due to improved SHFE/LME price ratios. However, high market offers led to significant disagreements between buyers and sellers, resulting in limited transactions. Additionally, market sources reported that long-term contracts for March-shipped seaborne cargoes continued to face delays, raising concerns about long-term supply.

(4) Secondary Copper: On March 17, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 72,900-73,100 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 2,175 yuan/mt, down 155 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,605 yuan/mt. According to the SMM survey, copper prices hovered at highs, keeping the price difference between primary and secondary copper rods above the advantageous threshold. Although the price difference between primary metal and scrap dropped back slightly, it did not affect traders' pick-up speed from last week. High copper prices also prompted wire and cable enterprises to consider increasing purchases of secondary copper rods. The secondary copper rod market saw a recovery in consumption, with some enterprises even reporting the need for production scheduling.

(5) Inventory: On March 17, LME copper cathode inventories decreased by 2,775 mt to 230,975 mt. SHFE warrant inventories increased by 5,453 mt to 163,102 mt.

Prices: Macro side, US retail sales for February recorded a MoM growth of 0.2%, below the expected 0.6%. The previous value was revised downward from -0.9% to -1.2%. The weaker-than-expected retail sales data caused the US dollar index to plunge, providing support for copper prices. Additionally, the OECD lowered its global economic growth outlook, revising the US 2025 growth forecast from 2.4% to 2.2%. Fundamentals side, on the last trading day of the 2503 contract, narrowing price spreads led to slightly improved morning transactions. However, copper prices climbed back above the 80,000 yuan/mt mark in the afternoon, significantly pressuring downstream consumption. With fewer imported copper arrivals in late March and limited domestic arrivals, spot discounts are expected to narrow slightly today. As of Monday, March 17, SMM reported that copper inventories in major regions across China fell by 6,500 mt from last Thursday to 349,000 mt, down 28,000 mt from the year's peak. Additionally, current national inventories are 46,400 mt lower YoY. In summary, with economic growth expectations revised downward and weaker-than-expected retail sales data, the US dollar index is expected to remain weak, keeping copper prices relatively firm today.

[The information provided is for reference only. This article does not constitute direct investment advice. Clients should make cautious decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.]